Fastest Ways to Catch Up on Your Retirement Savings

10 Min Read | Dec 9, 2025

Key Takeaways

- About half of Americans are not saving for retirement at all—and many feel behind on their retirement savings goals. If that’s you, it’s not too late to get back on track.

- If you’re debt-free and you consistently invest 15% of your income each month, you can put the power of time and compound interest to work for you and build a solid nest egg for retirement.

- Some of the fastest ways to catch up on saving for your retirement include maxing out your retirement accounts, looking for hidden savings in your monthly budget, and finding ways to increase your income.

- Turning your home into a powerful wealth-building tool or even pushing back retirement a few years can make a big difference by giving you more options in your retirement.

According to Ramsey Solutions’ State of Personal Finance study, about half of Americans are not currently investing for the future, and many of them feel behind on their retirement savings goals.

Market chaos, inflation, your future—work with a pro to navigate this stuff.

It’s time to wake up and get to work, people! And if you feel like you’re behind, fear not. We’re going to walk through a few ways you can catch up on your retirement savings.

But first, we want you to hear us say this: It’s never too late to get started saving for retirement. No matter how old you are or how much (or how little) you’ve saved so far, there’s always something you can do. You can’t change the past, but you can still change your future. The fat lady hasn’t sung yet!

Before we dive in, a quick warning—we’re about to throw a lot of numbers around (but in a good way). Ready? Let’s do this.

How to Catch Up on Retirement Savings

If you’re afraid to peek at your 401(k) balance or feel hopelessly behind on saving for retirement, it’s not too late to get back on track.

Let’s say you’re 40 years old with a $55,000 salary and you’re debt-free with an emergency fund in place. Not bad! But there’s just one problem—you have nothing saved for retirement. Since we recommend saving 15% of your gross income for retirement, that would mean investing $688 each month into your 401(k) and IRA. If you did that for 25 years, you could end up cracking the $1 million mark by the time you’re 65. That’s right—you would be a millionaire in 25 years!

But what if you don’t have 25 years? What if you’re 45—or even in your late 50s? Here’s the good news: You can take advantage of your age. People age 45–54 are in their peak earning years, and the average annual household income for that age group was $116,800 in 2024.1 If you invested 15% of that, you’d be putting away $17,520 per year (or $1,460 per month) for retirement.

If you stay focused on your retirement dream and continue investing $1,460 each month for 20 years, you could have more than $1 million saved for retirement! That’s the power of time and compound interest at work. You can run some numbers for yourself with our Investment Calculator, which will do all the math for you.

Now let's have a look at some practical things you can do to catch up on your retirement savings.

1. Max out your retirement accounts.

It’s not surprising that the vast majority of millionaires (80%) we talked to for The National Study of Millionaires said investing in their employer-sponsored retirement plans was the key for building wealth.

After all, 401(k)s, 403(b)s and other employer-sponsored retirement plans come with some amazing features that make them perfect for building a million-dollar net worth, like employer matching and tax-free or tax-deferred contributions and investment growth.

Employer-sponsored plans also have higher contribution limits that can help you. In 2025, you can invest up to $23,500 in your 401(k). A higher catch-up contribution limit adds $7,500 if you’re over 50 (for a total of $31,000). And if you’re age 60–63, your catch-up limit is even higher: If your plan allows it, you can contribute an additional $11,250 (for a total of $34,750).

And those numbers have increased for 2026. You can invest up to $24,500 into your 401(k), and the catch-up contribution (for those 50 or older) is an additional $8,000. If you’re age 60–63, your higher catch-up limit stays the same at $11,250.2

|

Plan Type |

Limit for Under Age 50 |

Catch-Up Contribution (Age 50 and Older) |

Maximum Total (Age 50 and Older) |

Catch-Up Contribution (Age 60–63) |

Maximum Total (Age 60–63) |

|

401(k), 403(b) |

$24,500 |

$8,000 |

$32,500 |

$11,250 |

$35,750 |

|

Traditional and Roth IRA |

$7,500 |

$1,100 |

$8,600 |

N/A |

$8,600 |

On top of all that, we haven’t even talked about your other secret weapon: the Roth IRA. For 2026, you can contribute up to $7,500 to an IRA outside of your workplace ($8,600 if you’re age 50 or older).3 Between your 401(k) and Roth IRA, you can really gain back some lost ground and make a comeback for the ages!

Now, if you’re wondering how you can do that, don’t worry—we’re going to show you some practical things you can do to start saving more for retirement today.

2. Look for savings in your monthly budget.

If you want to put more money toward retirement, you probably don’t have to look very far. Give yourself a goal to reach for by choosing a specific dollar amount you want to save. Maybe sit down with your spouse or an accountability partner and look for $250 you can shave off your budget.

Here are some quick ways you can potentially save hundreds of dollars:

- Cancel subscriptions and memberships. Do you really need Netflix, Hulu and Disney+? Pick one and dump the rest! The same goes for those gym memberships and magazine subscriptions.

- Cook meals at home instead of dining out. Americans spend almost $4,000 a year eating out at restaurants.4 That’s more than $300 a month for the average household! By cooking at home more often, you could save hundreds each month. Your wallet—and your waistline—will thank you.

- Get a better deal on car insurance. When was the last time you shopped around for car insurance? If it’s been a while, you might want to take a look. Those who compare rates and switch insurance can save hundreds of dollars on their annual premiums. Have an independent insurance agent shop around for you to see what kind of savings you can get!

Cutting things from your budget can be painful. You might need to give up your annual summer vacation to the beach or say no when your friends want to go eat at that fancy restaurant. But remember, you’re making short-term sacrifices that will help you retire on your terms—and that’s worth fighting for. You can do this.

3. Find ways to increase your income.

Your income is your number one wealth-building tool, so what better way to catch up on retirement than to grow it?

There are several ways to boost your income, including talking to your boss about a raise or promotion, working overtime at your current job, exploring new job opportunities, or even making a career change.

You could also start a side hustle to earn extra cash. From delivering pizzas on nights and weekends to tutoring schoolkids, there are plenty of options. Who knows—you might actually have fun!

And hey, got an extra room in your house? Rent it out. If your kids have launched for college or career, consider turning that space into a little extra income.

Whatever you choose, let’s say it brings in an extra $500 each month—what could that do for your nest egg? A lot.

Meet Dan. He’s 50 years old with $100,000 saved up for retirement. That’s better than nothing, but he still has a lot of work to do. Right now, he’s socking away $300 a month into his retirement savings. At that rate, he’ll have about $653,000 saved up for retirement by the time he turns 65.

But if Dan takes on a side hustle or rents out his spare bedroom and starts adding an extra $500 to his 401(k) and IRA each month—bringing his monthly contributions to $800—he could have $880,000 saved up at age 65. That’s about a quarter-million-dollar boost to his nest egg!

4. Turn your home into a wealth-building tool.

You may have a secret weapon to help you catch up on your retirement savings . . . and not even know it. In fact, you’re probably sitting in it right now. Yep, it’s your house!

According to the largest research study of millionaires ever done, the average millionaire pays off their home in 10.2 years. There’s a reason they knock out their mortgages early: Owning your home free and clear means entering retirement with another huge asset besides your retirement savings. That’s a simple way to diversify. And even better, paying off the house early frees up money you can use to supercharge your investing.

So, once you’re debt-free, one thing you can do to catch up on retirement is focus on paying off your mortgage as fast as you can while also investing 15% for retirement.

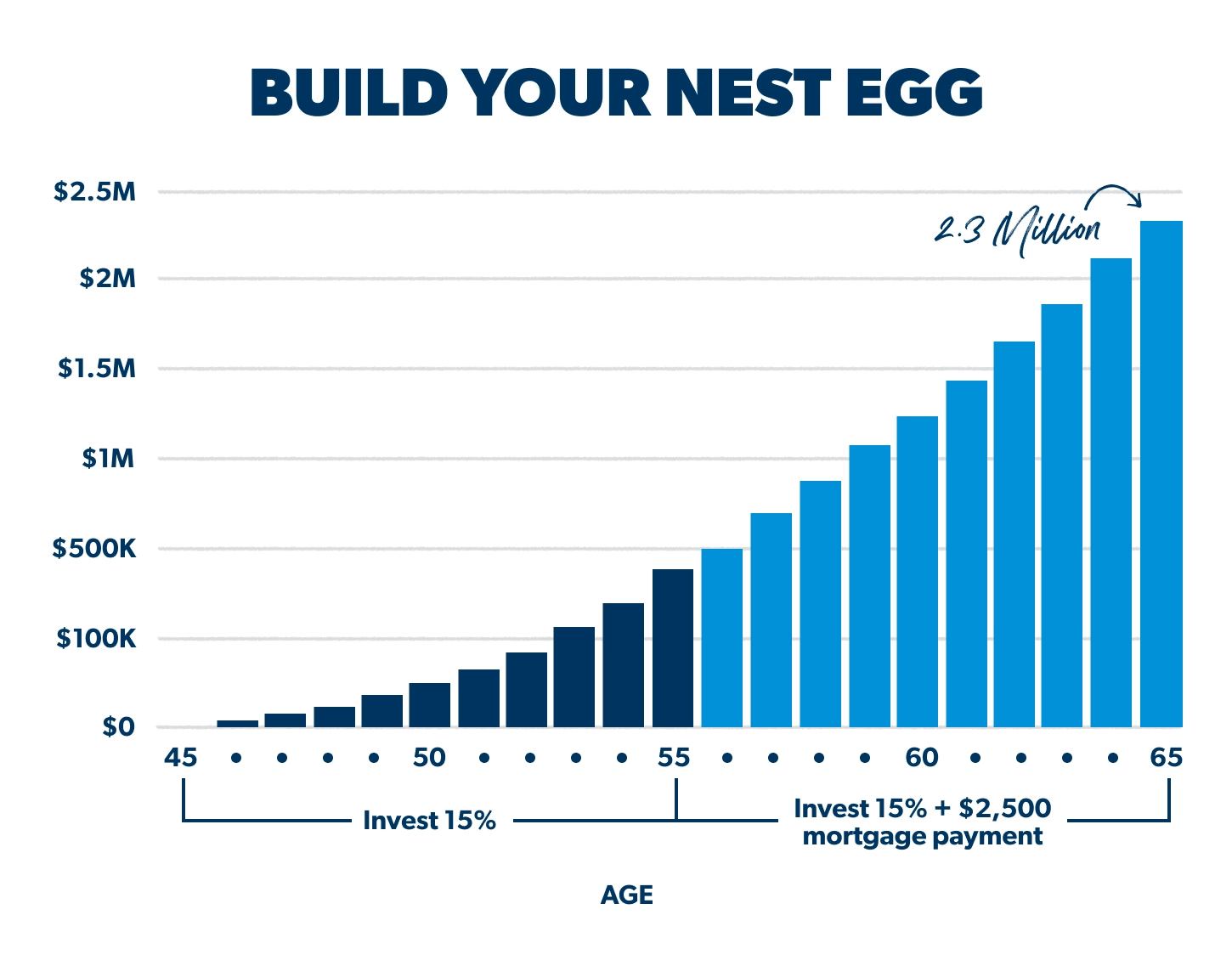

Let’s say you’re 45, debt-free, and married with two kids. Your net household income is $120,000 a year, and your mortgage payment is $2,500 a month. For the next 10 years, you invest $2,000 a month (15% of your gross income) for retirement, but you also commit to paying an additional $500 a month on your mortgage so you can pay it off by the time you turn 55.

In that 10 years, you could pay off your mortgage while also adding more than $434,000 to your retirement savings.

Now you’re 55, and the house is yours free and clear. With retirement right around the corner, you decide to put the pedal to the metal for the next 10 years. So, you increase the amount you save each month by $2,500—your old mortgage payment. Now you’re contributing not $2,000 but $4,500 a month. In that final 10 years before retirement, by investing even more in your 401(k), your total retirement savings could be $2.3 million!

So, in 20 years (from age 45 to 65), your retirement vision becomes reality. You’ve got a paid-for home and a nice nest egg waiting for you—because you stayed focused on your long-term goal and worked hard to get there.

Pro Tip: A paid-for house gives you options! You could sell your paid-for home, use a portion of the proceeds to buy a smaller home with cash—and put the rest toward your retirement.

5. Push back retirement a few years.

Uh-oh. We can practically hear the grumbles from across the internet now. But hear us out: If you feel like you’re really behind, what if, instead of retiring at 65, you kept saving and working until age 70? That gives compound interest five more years to do its thing, and those five years can make a world of difference.

Working longer isn’t an option for everyone. But if you’re in good health and enjoy what you do, staying on the job a little longer can be a great choice—for your mental health and your finances.

If you invest $800 a month from age 45 to 65, you could end up with close to $700,000 in your nest egg. That’s not bad! But if you stay focused and keep working and investing at that same rate for five more years, your retirement savings could grow to $1.2 million. That’s compound interest working its magic!

Work With an Investment Professional

If you’re late getting into retirement investing, there’s still time—and it’s still worth it. But you need to know that it’s time to get intense and start building habits that will help you get where you need to go.

That’s why you need to work with an investing professional you can trust. Our SmartVestor program can connect you with an investing pro who can help you understand your options and lay out a plan for your retirement. Age is a number, not an excuse. You can start making progress today!

Next Steps

- If this article was a good start but you still have questions, check out the Ramsey Investing Hub. You’ll find free tools—like the Retirement Assessment and Investment Calculator—to help you estimate how much money you’ll need to retire on your own terms.

- Grab a copy of Dave Ramsey’s bestselling book Baby Steps Millionaires and learn how to bust through the barriers preventing you from building wealth.

- Investing can feel complicated and overwhelming, but you don’t have to tackle these challenges alone. The SmartVestor program can connect you with an investment pro who can help you set retirement goals and get started investing.

Make an Investment Plan With a Pro

SmartVestor shows you up to five investing professionals in your area for free. No commitments, no hidden fees.

This article provides general guidelines about investing topics. Your situation may be unique. To discuss a plan for your situation, connect with a SmartVestor Pro. Ramsey Solutions is a paid, non-client promoter of participating Pros.

Get Weekly Insights Delivered Straight to Your Inbox

Did you find this article helpful? Share it!

About the author

Ramsey Solutions